The Sunday Signal: Capital Doesn’t Lie

IBM fell 13%. Atlassian is down 73% over 52 weeks. Block cut 40% of its workforce and the market cheered. Three signals. One direction. Issue #43 | The Sunday Signal | Sunday, 1 March 2026

Bottom Line Up Front

Last week’s issue, The Loom, the Layoff, and the Life Raft, made the historical case. From Yorkshire’s handloom weavers to the junior developers of 2026, the pattern was clear. Skilled work gets eaten by machines. The people in the middle convince themselves it is temporary.

The response in my inbox was predictable. Developers telling me AI hallucinates. Lawyers explaining it still needs supervision. Professionals arguing it is not production-ready.

That may all be true.

But when I want to know whether something is real, I do not start with opinions. I start with markets.

Commentary is frictionless. Capital is not.

Financial markets are where pension funds, sovereign wealth, boards and institutions reprice assumptions with real money at stake. When billions are marked down in a single session, something structural has shifted.

This week, three separate corporate stories told the same story.

AI has stopped being a productivity narrative. It is becoming a cost narrative.

And the market is confirming it.

Part One: The Triple Warning Shot

IBM and the fragility of “complexity”

On Monday 23 February 2026, IBM’s shares fell roughly 13% in a single trading session. Its worst single-session fall in over twenty-five years.

That is not a routine wobble. That is a repricing event.

IBM’s modern business is built heavily on consulting and legacy modernisation. For decades, the complexity of COBOL estates inside banks and governments acted as a moat. Untangling forty years of accumulated business logic required armies of specialists. That slowness was billable.

Whether that claim proves fully accurate is secondary. The market heard something simpler.

Complexity might no longer be scarce.

If the moat weakens, the margin compresses. Public markets do not wait for certainty. They discount direction.

Thirteen per cent in a day is what direction being repriced looks like.

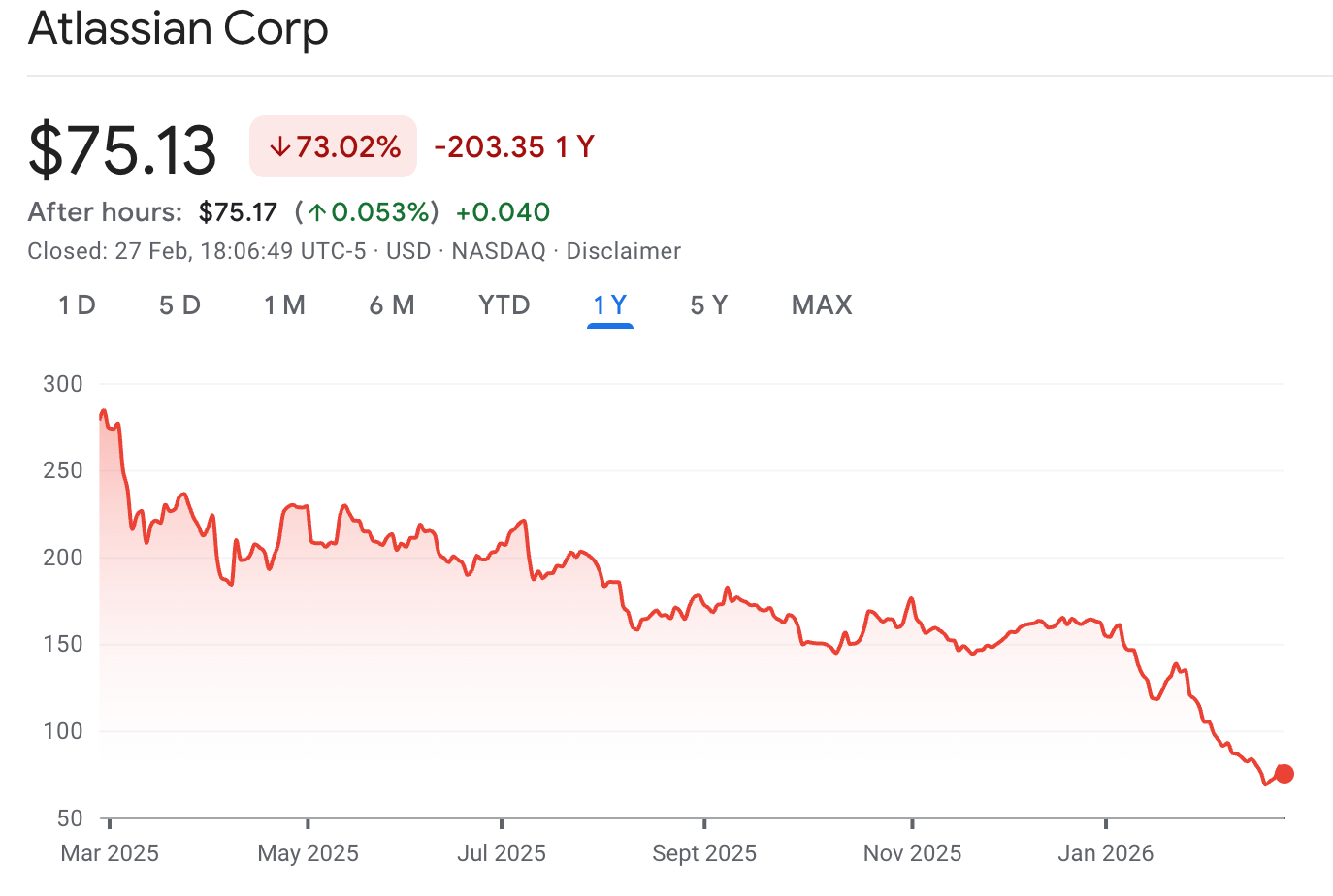

Atlassian and the end of the per-seat assumption

Over the past fifty-two weeks, Atlassian has been widely reported as down roughly 73%, trading near levels last seen in 2018.

Strip away macro noise and a cleaner question emerges.

Atlassian’s model is built on seats. Seats track headcount. Headcount is the input.

If AI increases output per engineer materially, companies need fewer engineers. If they need fewer engineers, they need fewer seats.

When input shrinks structurally, revenue assumptions shift structurally.

This is not about Jira features. It is about labour intensity. And it matters beyond Atlassian. There is an entire category of SaaS businesses whose revenue assumptions are built on human headcount at the companies they serve. The per-seat pricing model that defined a generation of cloud businesses is being repriced in real time. The transition will be brutal for the companies caught in between.

Block and the incentive structure

On Thursday, Jack Dorsey announced that Block would cut over 4,000 employees, roughly 40% of its workforce, explicitly linking the restructure to intelligence tools. The company is profitable. It is growing. No crisis. No failed product.

Shares jumped roughly 25% in after-hours trading.

That is not sentiment. That is capital signalling approval.

Every board in the developed world just saw a case study: reduce headcount aggressively, attribute it to AI efficiency, get rewarded.

The copycat cycle has begun.

Part Two: This Is How We Now Build at Yorkshire AI Labs

Let me be precise.

This is not speculation about the future of software. This is how we now model and capitalise companies inside the Yorkshire AI Labs portfolio.

Three years ago, a new software venture followed a predictable structure. Core development squad of six. UI and front-end another six. QA and testing another six. DevOps and release engineering another six. Twenty engineers before meaningful traction was considered normal. Investors expected it. Headcount signalled seriousness.

Now we increasingly structure around one highly capable AI-native engineer at the centre of the build.

One.

Not because we are cutting corners. Because the economics have changed.

Even in Yorkshire, a fully loaded engineer costs roughly £80,000 to £100,000 per year once salary, national insurance, pension, tooling and overhead are included. Twenty engineers means £1.6 million to £2.5 million annual burn before product-market fit. Under our current portfolio model, a single AI-native engineer, properly tooled, can orchestrate generation, testing, documentation, deployment and integration work that previously required multiple squads.

The cost base collapses. Runway extends. Dilution reduces. Capital efficiency improves dramatically.

That is not theoretical. It is how we are allocating capital today.

A Live Portfolio Example

A CTO in one of our portfolio companies recently needed to replicate a major bank integration environment. APIs. Error handling. Rate limiting. Latency behaviour.

Historically, that would have required weeks of structured engineering work.

Using AI tooling, he generated a functioning mock banking environment in minutes. He reviewed it, validated it and moved straight to live integration.

Four weeks became minutes - literally.

When you see that inside your own portfolio, you understand why public markets are moving.

The Pattern Across Our Portfolio

The banking example is one instance. The pattern repeats.

A fintech building KYC compliance tooling used to need a legal team, a compliance team and an engineering team working in parallel. Now one AI-augmented compliance engineer produces a first-draft mapping from regulation text to technical specification in hours. The parallel-squad model has collapsed into a sequential, much leaner process.

A health-tech company building NHS data integrations used to require specialists in HL7 FHIR standards who took years to develop that specialism. Now AI surfaces the relevant standards, generates the integration schemas and flags known edge cases, compressing the learning curve dramatically.

A B2B SaaS company building workflow automation used to need separate product, research and engineering teams. Now, a two-person team does the work that previously required ten.

This is what last week’s issue called the Slow Squeeze. Wages under pressure first. Status following. The profession reorganising around fewer people. This week’s three market signals are what the Slow Squeeze looks like when it hits a public market all at once.

Part Three: The K-Shape. Which Side Are You On?

Understanding what is happening at the macro level is one thing. The more important question is what it means for the individual.

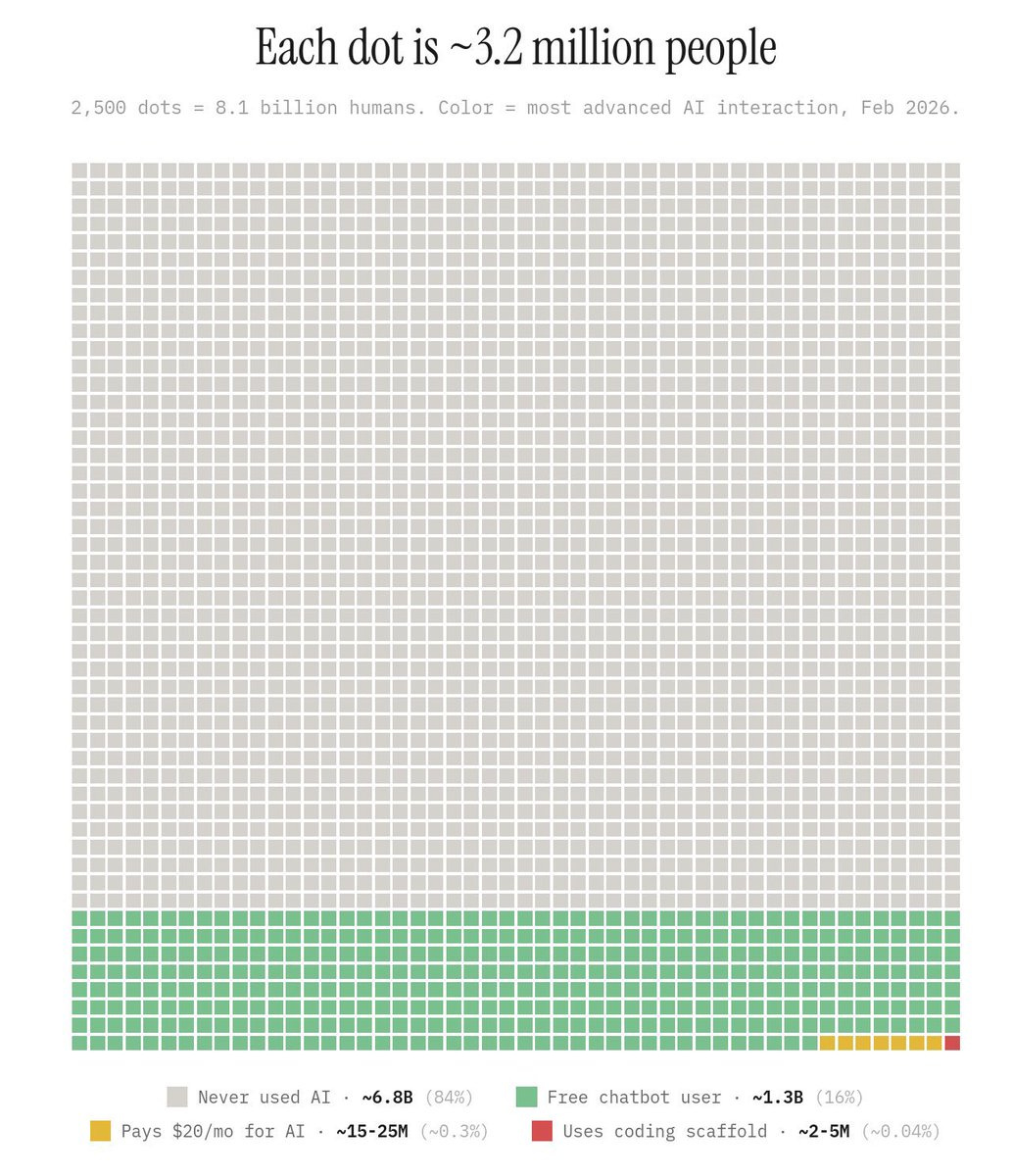

Miles Deutscher has been writing about what he calls the K-shaped AI economy: one diverging trajectory where those who master AI compound their advantage, and another where those who do not are gradually managed out. A visualisation circulating widely this week, a dot matrix attributed to Damian Player, CEO of Agent Integrator, puts the adoption split into stark relief:

Each dot represents 3.2 million people. The full grid is 8.1 billion humans alive today.

Of those 8.1 billion, approximately 84% have never meaningfully used AI. The revolution, for most of the planet, is still entirely abstract. Another 16% are free chatbot users: occasional, modest, competitive advantage thin and eroding. Approximately 0.3%, some 15 to 25 million people, pay for AI tools and are gaining genuine efficiency advantages. And at the absolute frontier, roughly 2 to 5 million people, 0.04% of humanity, are using coding scaffolds to build: deploying tools like Cursor, Bolt, or Claude Code to create their own applications, automations and infrastructure.

That last group is the Red Dot. The gap between the Red Dot and everyone else is widening at an accelerating rate.

The Four Baskets

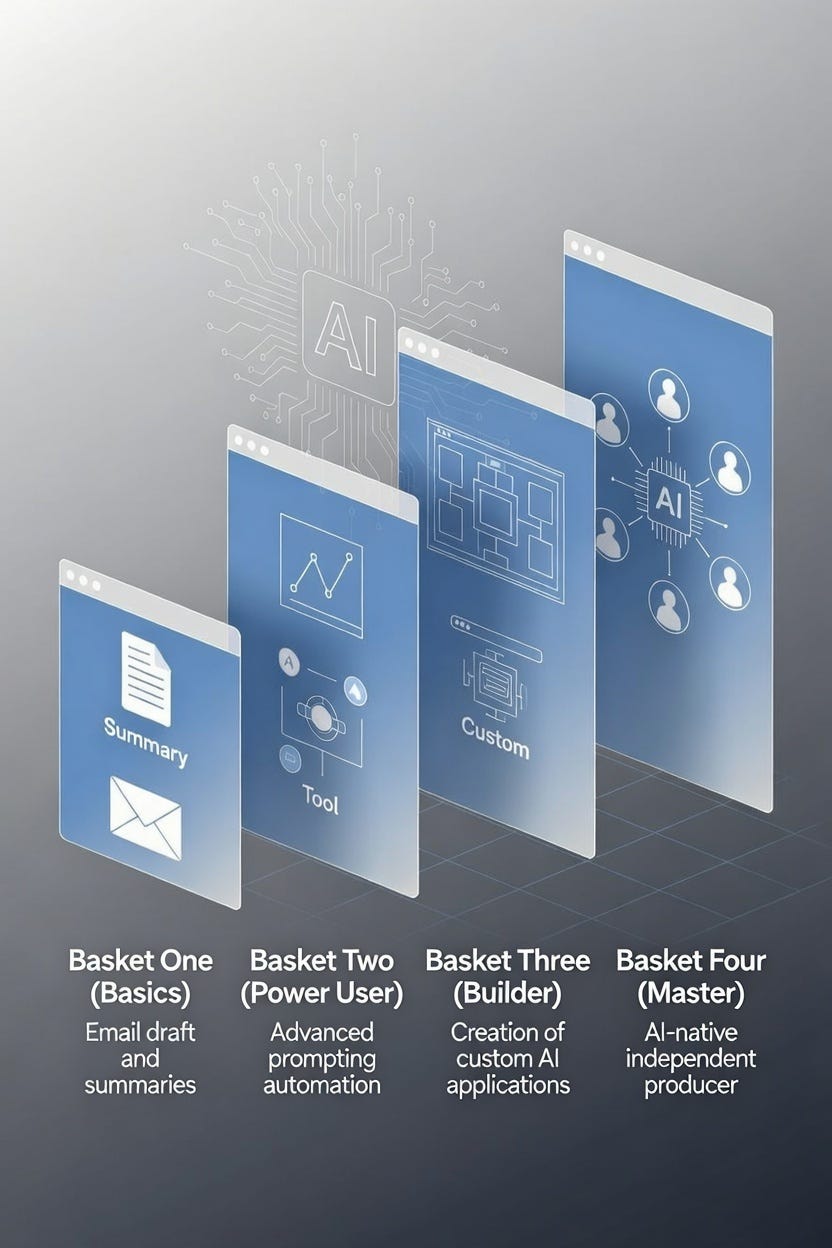

Deutscher maps individual AI capability into four levels.

Basket One: The Basics. Using AI for summaries, research, draft emails. Most people who use AI at all are here. It saves time. But as a competitive differentiator, it is rapidly approaching zero. If everyone can summarise a document with a chatbot, doing it with a chatbot confers no advantage. These skills are being commoditised in real time.

Basket Two: The Power User. Advanced prompting. Multi-step agentic workflows. Automating sequences of work without manual intervention at each step. At this level, you genuinely do the work of two or three people. The efficiency gain is real. But the uncomfortable truth: you are still an employee, still trading time for money, still vulnerable to the next efficiency leap that makes your current toolkit look basic.

Basket Three: The Builder. This is where things change qualitatively. You are using coding scaffolds to create your own applications, your own automations, your own solutions to your own problems. You stop being a consumer of other people’s software and start being a producer. You build tools that did not previously exist, in hours rather than weeks. You are no longer dependent on the off-the-shelf tool market. You create bespoke capability at low cost.

Basket Four: The Master. AI-native businesses. Consulting. Distribution. The connection between time spent and income earned is fully broken. You are building systems that operate without you. The IBM signal, viewed from Basket Four, is not a threat. It is an opportunity. The COBOL modernisation work that IBM charged armies of consultants to do is now available to a single AI-native practitioner with the right tools and the right clients.

Most professionals reading this are in Baskets One or Two. The direction of travel matters more than the current position. The window to move up is narrowing. Not closing. Narrowing.

The Ladder Is Being Pulled Up

The entry-level roles that once trained professionals, the junior analyst, the graduate developer, the trainee paralegal, are the first to go. Not because AI does their work perfectly. Because AI does it well enough, cheaply enough, quickly enough that companies are no longer willing to pay a human to do it while they learn.

Professional development has always worked through apprenticeship. You start at the bottom. You do the grunt work. You accumulate the judgment and contextual knowledge that makes you valuable at the senior level over the years. The junior role was not just a job. It was the training ground for the senior role.

If the junior role disappears, the training ground disappears with it. The people who climbed that ladder got something that will not be available to the next generation. The ladder is being pulled up behind them.

Last week’s issue made the point from history: the handloom weavers also had genuine expertise. The new categories of work in the textile industry were not available to them. The transition, though not instantaneous, was fast enough to destroy a generation.

Deutscher’s argument is that we are in a 6 to 12-month window where the gap between the two trajectories of the K is still bridgeable. After that, the compounding advantages of the Red Dot become structurally difficult to close.

The timeline is debatable. The direction is not.

What You Can Actually Do

The analysis is only useful if it leads somewhere actionable.

The first move is the mindset shift from passive observer to active experimenter. Most people in Baskets One and Two are using AI the way people used early search engines: to find information faster, not to build new capability. That framing limits what you can learn and what you can build.

The second move is systematising your exposure. The people getting ahead are not occasional readers of good AI articles. They have a daily or weekly discipline around understanding what is now possible: research announcements, developer communities, product releases that signal new capabilities. Not to become technical experts. To understand what tools now exist before those tools become mainstream knowledge.

The third move, the one that separates Basket Two from Basket Three, is to build something. Anything. A custom automation for a task you do repeatedly. A tool specific to your work. A dashboard that aggregates information you currently gather manually. The act of building with AI tools transforms your understanding of what is possible. It moves you from consumer to producer, which is exactly the distinction the market is beginning to price.

The fourth move is positioning. The Red Dot individuals are connected to other builders, other AI-native practitioners, other people using these tools seriously. The networks forming around AI-native practice are becoming economically significant. The people inside them are getting access to opportunities and knowledge not visible from outside.

The IBM signal, the Atlassian signal, and the Block signal are all pointing in the same direction: companies are restructuring around fewer, higher-capability humans deeply integrated with AI. The people who survive and thrive are the ones who made themselves irreplaceable by becoming builders rather than users.

Final Thought 🚀

Last week set out the historical pattern. This week, the market confirmed it.

IBM’s repricing. Atlassian’s long decline. Block’s headcount reduction rewarded by investors.

Three separate stories. One structural signal.

When the cost of producing digital output falls, labour intensity falls. When labour intensity falls, margins shift. When margins shift, valuations move.

The machine did not need to be perfect. It needed to be cheaper and capable of improvement. By the time it closed the quality gap, the industry had been rebuilt around it, with far fewer people, different skills, and no apology for the transition.

Opinions are frictionless.

Markets are not.

Capital has started to move.

The window is open. For now.

Until next Sunday, David

David Richards MBE is a technology entrepreneur, educator, and commentator with over 25 years in technology. He writes for the Yorkshire Post and publishes The Sunday Signal weekly at newsletter.djr.ai