The Sunday Signal: The Consultants Are Selling You a Lie

Gartner sells reassurance. Huang is building replacement. The Sunday Signal | Issue #48 | 5 April 2026

Bottom Line Up Front

The consulting industry has a structural incentive to tell CEOs that AI is a transformation story rather than a replacement story. Transformation sells tools, training and advisory retainers. Replacement triggers severance plans and ends the relationship.

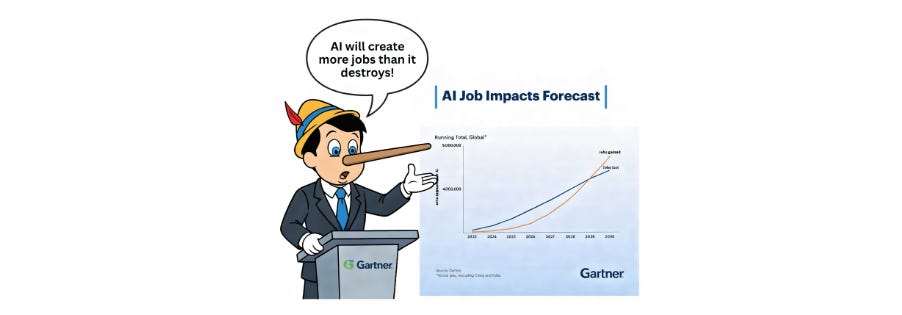

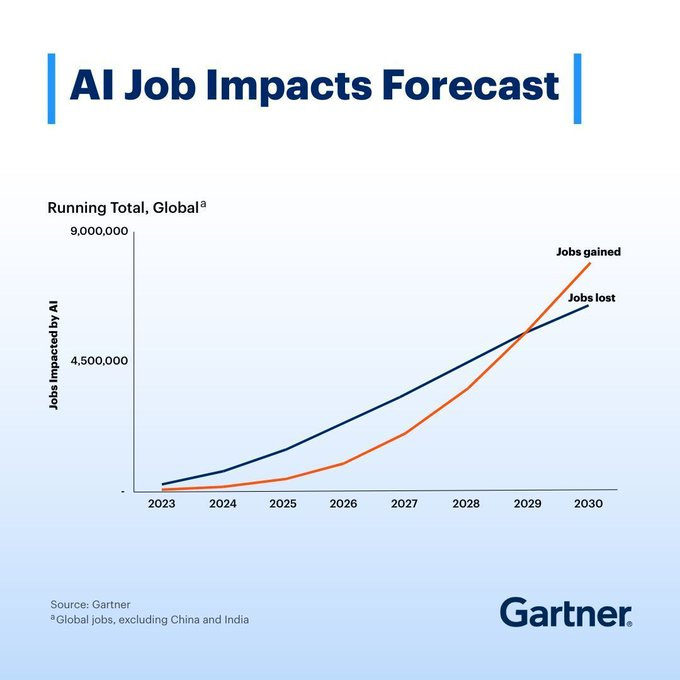

Gartner’s November 2025 forecast tells six thousand CIOs that AI will create more jobs than it destroys. It promises amplification, not elimination. It is a compelling narrative.

It is also wrong in four specific ways.

While that message was being sold in Barcelona, Jensen Huang stood in New York and described a world where all software becomes agentic. Not assisted. Autonomous.

At the same time, one of my team built a company from conversation to live website in sixty minutes. Not a demo. Not a concept. A functioning business ready for customers.

These three realities cannot all be true at once.

Listen to this issue as a podcast. Available on Spotify, Apple Podcasts, and YouTube.

1. The Four Failures Inside Gartner’s Jobs Forecast

Gartner’s headline from the November 2025 IT Symposium was this: starting in 2028, AI will create more jobs than it destroys. By 2030, they predict that twenty-five per cent of IT work will be done by AI alone, seventy-five per cent by humans augmented with AI, and zero per cent by humans without AI involvement. Their recommended response is to “restrain new hiring” for low-complexity roles and “reposition talent” toward higher-value work.

It sounds reasonable. It is not. Here are four reasons why.

The junior talent pipeline is a death spiral Gartner refuses to name.

Entry-level, low-complexity work is not a category of expendable busywork. It is the apprenticeship. It is where the next generation of senior professionals learns how organisations actually function, how to make decisions under pressure, how to handle being wrong in a client meeting, how to develop the judgment that cannot be learned from a training manual. Gartner recommends CIOs automate this rung.

Remove the rung and the ladder disappears. No ladder, no experts. No experts, no “augmented workforce.”

The efficiency-creates-volume assumption is a fallacy built on infinite demand.

The “new jobs” argument rests on an economic assumption that held during the Industrial Revolution but does not hold in finite knowledge markets: that if a task becomes ten times cheaper and faster, we will simply do ten times more of it. If an AI can handle every first-line IT support ticket for a five-thousand-person organisation, that organisation does not hire ten times the support staff to process ten times the volume. It retains two people to oversee the system and eliminates the other thirty.

That is not transformation. That is subtraction.

The workslop problem is accelerating, not resolving.

Gartner’s own analysts admitted in Barcelona that “humans are less ready to capture value” from AI and warned about skills atrophy as workers offload tasks to machines. What they did not say is that the practical consequence is already a proliferation of AI-generated output of insufficient quality: code that compiles but breaks, analysis that sounds authoritative but is wrong, documentation that is grammatically correct and factually hollow. Fixing, verifying, and securing this output frequently takes more human time than creating the original would have done.

The job becomes checking the machine. That is not augmentation. It is degradation.

Historical precedent is the wrong map for this territory.

Optimists reach, inevitably, for the car and the horse. The automobile killed carriage-making and created automotive engineering. Disruption created new categories of skilled work. Therefore, AI will do the same. The problem with this analogy is structural. Every previous wave of automation moved human labour up the value chain: from physical to cognitive, from manual to managerial. AI targets cognition itself. There is nowhere further up to go when the machine can already reason, code, write, synthesise, and analyse at a level that exceeds the median knowledge worker. Nobel laureate Daron Acemoglu has named this “So-So Automation”: technology that is precisely good enough to replace a human but not good enough to spark the next economic boom. It raises margins while hollowing out the middle. That is not progress. It is compression. Gartner does not mention Acemoglu.

A brief record of Gartner’s forecasting accuracy.

Before investing heavily in Gartner’s 2030 vision, it is worth reviewing their track record.

In 2011, they predicted Windows Phone would hold over twenty per cent of the global smartphone market by 2015. Windows Phone died at approximately two per cent. In 2017, they placed blockchain at the “Peak of Inflated Expectations” in their Hype Cycle and predicted it would generate over three trillion dollars in business value by 2030. By 2019, they were acknowledging that ninety per cent of enterprise blockchain projects had failed to leave the pilot stage. They predicted tablet sales would reach four hundred and fifty million units annually by 2016 and that the PC was heading for obsolescence. Tablet sales peaked and declined; the laptop survived.

The pattern is consistent. Gartner predicts possibility, not reality. Adoption, timing, and consequences are where they fail. And they are chronically biased toward the optimism of the audience writing the cheques. If you tell a CIO that AI will replace twenty-five per cent of their labour costs, they consider buying the software. If you tell them it will create twenty-five per cent more jobs, they buy it and feel progressive about it. The second story converts better. Gartner knows this.

2. Jensen Huang Did Not Come to Comfort You

On 4 March 2026, Nvidia’s CEO appeared at the Morgan Stanley Technology, Media and Telecom Conference in New York and said something that should have ended the Gartner conversation.

“There will be no software in the future that is not agentic. How could you have software that is dumb? And so, it is absolutely true that every software company will become an agentic company.”

Not some software. Not enterprise software. Not AI-native software startups. Every software company. All of it.

Huang’s argument is structural. The SaaS model, in which software is a passive tool licensed by the seat and operated by human hands, is already obsolete in its architecture. The future is software that receives an instruction, reasons about what to do, and executes it without human intervention at each step. His direct comparison was to workforce management: just as companies today manage a mix of full-time staff, contractors, and specialists, they will soon manage a portfolio of proprietary internal agents and externally rented agents, each deployed for specific tasks.

The business model implication is significant. Today’s software companies sell licences. Tomorrow’s will “rent out agents to do work” and sell “specialised tokens” representing specific expertise and output. Value no longer sits in the code. It sits in the outcome the agent delivers.

Huang also confirmed that Nvidia will invest thirty billion dollars in OpenAI, describing this as likely their last opportunity to invest before the company goes public. Their ten-billion-dollar position in Anthropic may also be a final private-market stake. These are not hedging gestures. They are bets on the companies whose foundation models will power every agentic system built over the next decade, running on Nvidia’s hardware.

Gartner is describing a transition. Huang is describing an endpoint.

The irony is visible if you look for it. In November 2025, Gartner presented to six thousand CIOs that the future would be “humans amplified by AI, orchestrated by the CIO.” Fourteen weeks later, the man building the infrastructure that future runs on said clearly that there will be no software left that does not think for itself. In Huang’s architecture, the CIO does not orchestrate the system. The system orchestrates itself.

3. The Moat Has Gone. Some People Have Not Noticed Yet.

This week I published a column in the Yorkshire Post making a straightforward argument: the economic foundation of the SaaS industry is collapsing. Not at the edges. At the centre.

The evidence was concrete. One of my team sat with a founder for a conversation. That conversation, fed into Claude, became a detailed business plan. The plan went into Claude Code and became a working prototype and a website. Sixty minutes, start to finish. No committee. No developer. No specification cycle. No design sprint theatre. A company, ready to talk to customers.

The piece generated twenty-six thousand LinkedIn impressions within twenty-four hours, a hundred and nine comments, and a response from a cross-section of people that told you more about the state of the industry than any Gartner survey.

Some understood immediately. One commenter observed that the software moat had been draining for some time and that AI had simply pulled the plug. Another made the point that speed to prototype removes the theatre and forces the truth: the first real test of a business is whether someone pays. A third noted that the moat was always distribution and trust, not the code itself, and that it had simply taken this moment for that to become undeniable.

But a significant portion of the responses came from people who are not yet ready to accept what they are looking at. One called the piece “attention-grabbing hyperbole” and demanded to be shown a company created in an hour that used to take twelve months. Another questioned how I could feel “comfortable” making the claim. A third dismissed it as “lazy slop written by AI, devoid of humanity.” One, deploying a form of reasoning that will be familiar to anyone who has followed previous technological shifts, argued that because Microsoft and Salesforce remain large companies, the entire argument is false.

I understand the instinct. When your professional identity is built on the assumption that software requires years of training, expensive tooling, and specialist teams to produce, the idea that a conversation and a lunch hour can replicate the output is not examined. It is rejected.

But one comment stood out for its honesty. A Director of Engineering observed that code has never been a moat. He is right. What the SaaS industry sold was not code. It sold accumulated complexity, switching cost, and the time required to build an alternative. AI has compressed the time. It has not eliminated the complexity of building a genuine business: you still need customers, revenue, operational infrastructure, and the thousand unglamorous things that happen after a prototype exists. But it has moved the fundamental question from “can anyone build this?” to “why would anyone pay for this when they can build it themselves?”

For a great deal of existing SaaS, the answer is increasingly: they would not.

Salesforce is not dead. The long tail of SaaS, the thousands of competent point solutions charging twelve seats a month for something a capable team can now assemble in an afternoon, is a different story. Huang told you where that story ends. Gartner will tell you it ends in a jobs boom. One of them has financial skin in the game. The other is building the machine.

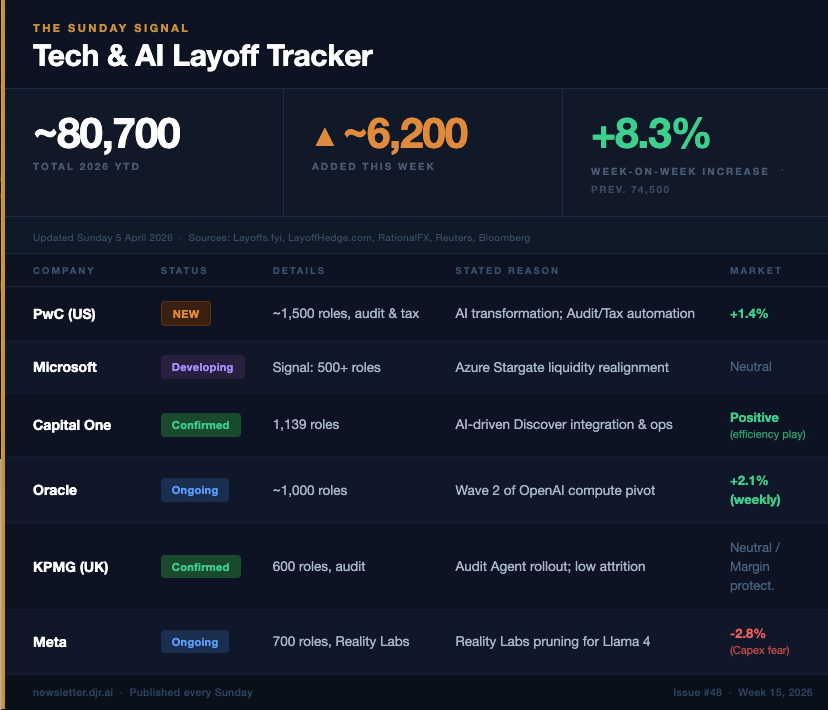

The Sunday Signal Tech and AI Layoff Tracker | Week 15 | 29 March -- 4 April 2026

2026 Year-to-Date Total: approximately 80,700 Week-on-Week: up from approximately 74,500 Added This Week: approximately 6,200

Data: Layoffs.fyi and tracker-based estimates. For informational purposes only.

The Signal: The Stargate Squeeze

Microsoft is entering a critical phase. The Stargate supercomputer funding timeline is creating internal pressure visible not in headline announcements but in quiet reductions across non-AI divisions: hardware teams, secondary Azure services, roles that cannot be directly mapped to the OpenAI project cost structure. This is how large restructurings now happen. Not in headlines, but in drift. When cuts are too small to announce, they are often too large to miss.

The Audit Agent Domino Effect

As anticipated, the threshold has been crossed. PwC confirmed approximately fifteen hundred US roles cut, targeting audit and tax departments specifically.

This is not a restructuring. It is a structural collapse of a business model. The Big Four pyramid has always relied on an army of junior graduates performing manual verification at scale: matching invoices to purchase orders, checking figures against source documents, flagging exceptions for senior review. The Audit Agent does not sample one per cent of transactions. It processes one hundred per cent in real time, via direct API access to ERP systems, using fine-tuned models trained on decades of GAAP and IFRS documentation. By tracker-based estimates, the work that previously required five thousand graduates annually is now approximately ninety-nine per cent automated.

The professionals who remain are not accountants. They are AI systems auditors. Their function is to verify that the agent has not suffered logic drift, that its reasoning chains connect cleanly to source data, and that no client has inadvertently instructed the system to overlook categories of loss. If you cannot read the traceability map of an AI’s decision, you are a legal liability to the firm, not a value contributor.

The human role has shifted entirely: from doing the task to auditing the system that does the task. That shift requires a fundamentally different skill set. Most of the people currently doing the task do not yet have it.

Market Divergence: The Efficiency Premium

The market continues to price “brutal logic” as a premium signal. Oracle rose 2.1 per cent on confirmed cuts. Capital One’s reductions were received positively. The arithmetic is simple: investors are treating payroll as technical debt being successfully converted into productive compute.

Meta tells the opposite story. Seven hundred Reality Labs cuts were met with a sell-off. Investors are no longer questioning Meta’s headcount decisions. They are questioning whether the one-hundred-and-thirty-five-billion-dollar compute bill can be justified against revenue. Cutting humans is no longer sufficient reassurance. The direction of the cuts matters.

High-Probability Targets: Week 16

Salesforce carries the highest risk profile on the tracker. Agentforce 2.0 has reached internal peak maturity, and BDR and SDR roles are the logical next liquidation target as the company moves toward an automated sales funnel. Deloitte must match the PwC and KPMG moves to maintain competitive audit pricing. Alphabet faces a projected one-hundred-and-eighty-five-billion-dollar Capex requirement against a Gemini user base not yet sufficiently monetised. ServiceNow’s CEO has publicly claimed ninety per cent automation of back-office support, which means those roles are operating on borrowed time.

Labour is the new interest expense. In 2026, every person on a payroll is a unit of liability to be justified against the performance of an AI agent. The justification is becoming harder to make.

Final Thought

Gartner will update its forecast next year. It will include new charts, new language, and new frameworks to explain decisions that have already been made.

Huang is not publishing forecasts. He is building the outcome.

The gap between those two things is where entire careers disappear.

Most people will not notice until they are inside it. 🚀

Until next Sunday, David

David Richards MBE is a technology entrepreneur, co-founder of Yorkshire AI Labs, and a weekly columnist for the Yorkshire Post. The Sunday Signal publishes every Sunday. If someone forwarded this to you, you can subscribe at newsletter.djr.ai

Listen to this issue as a podcast. Available on Spotify, Apple Podcasts, and YouTube.