The Sunday Signal: The Army Has Become the Liability

Twenty-five employees. One hundred million dollars. And the toolkit costing under £3,000 a month that is making traditional companies obsolete. Issue #45 | 15 March 2026

The Bottom Line Up Front

45,724.

That is the number of tech and AI-related roles eliminated or reported for elimination in 2026 so far, according to tracker-based estimates from RationalFX and Layoffs.fyi. We are not yet through the first quarter.

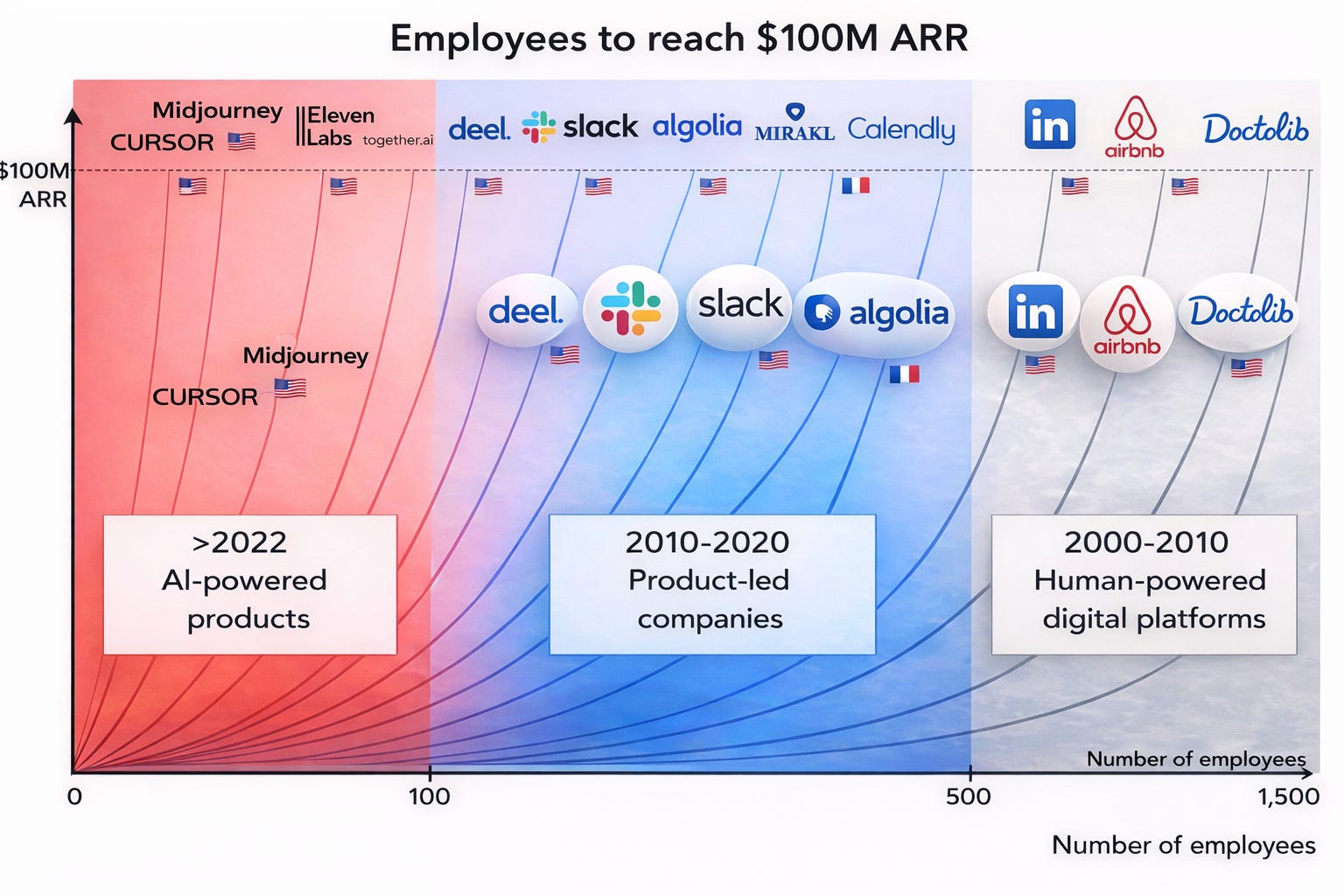

Twenty-five employees. One hundred million dollars in recurring revenue. Achieved in twelve months, with no marketing budget, by a team of engineers and founders that would not fill a typical company’s finance department.

That is what Cursor looked like when it hit a milestone that once implied an entire mid-sized company. That is not a curiosity. It is a warning.

This week’s issue has three parts. First, the Yorkshire Post column: the one-person unicorn is coming, and most business leaders still do not grasp the scale of the change. Second, the mechanics: how AI-native companies are replacing headcount with agents in engineering and go-to-market. Third, the stack: the tools making this possible, and why the cost of testing a serious company idea has collapsed.

And from this week, The Sunday Signal adds a permanent new section: The Sunday Signal Tech and AI Layoff Tracker.

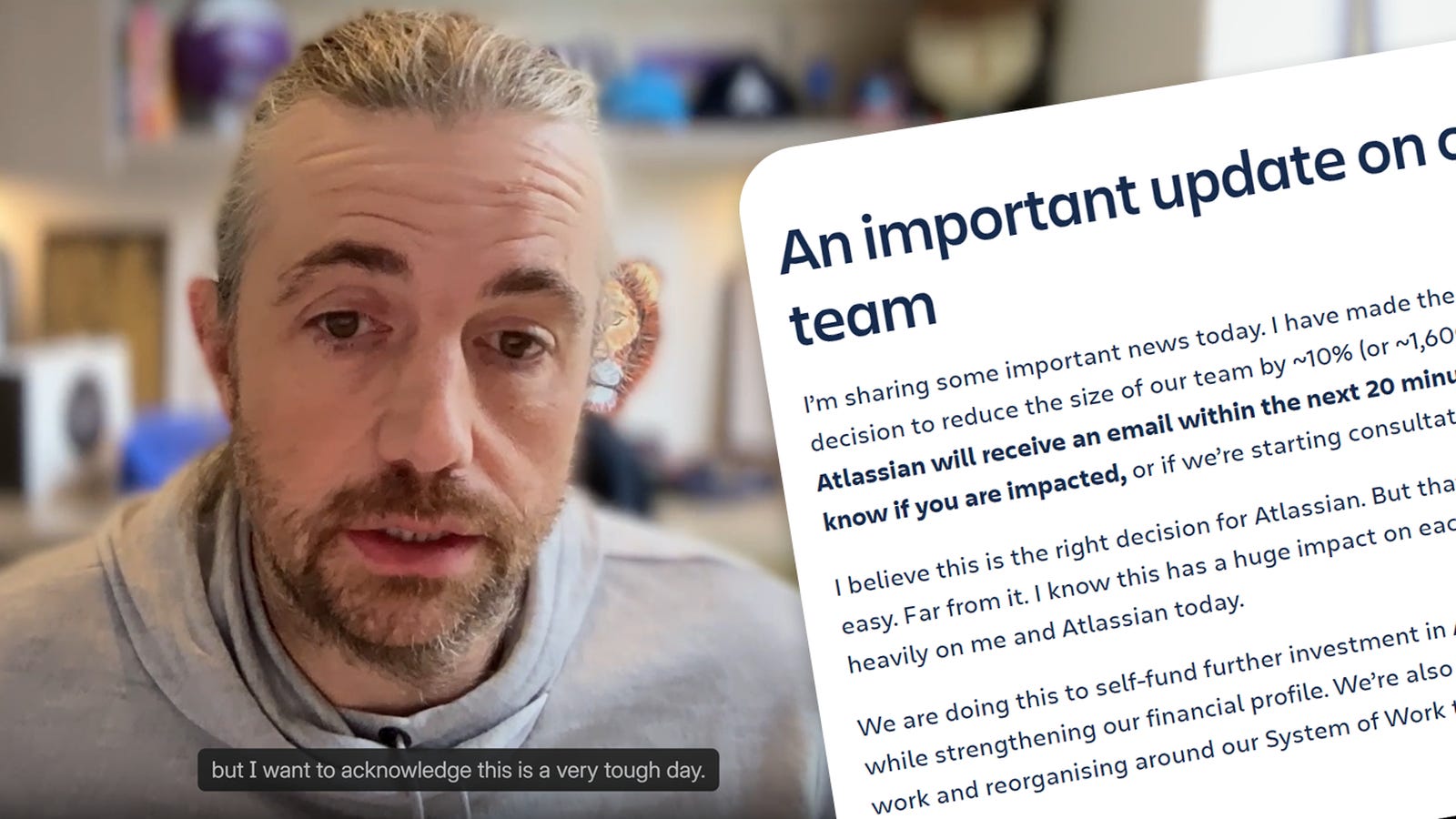

The numbers demand it. Atlassian cut 1,600 roles on 11 March. Block cut over 4,000 in late February. WiseTech cut 2,000. Amazon is rolling through 16,000 corporate positions. In every confirmed case, management is making the same strategic bet: fewer people, more automation, more AI leverage. In every confirmed case, investors responded by pushing the share price up. Block surged 25 per cent on the day. WiseTech jumped 11 per cent. Atlassian rose between 2 and 4 per cent.

The market is not mourning these jobs. It is pricing in the leverage.

I have been building to this section since Issue #40 on 8 February. The data has been accumulating week by week. It now has its own space, every Sunday, for as long as this wave continues.

You can also listen to The Sunday Signal as a weekly podcast using a voice cloned from my own voice, a demonstration of the same AI capabilities I write about. Listen on Spotify, Apple Podcasts, and YouTube.

Story One: The One-Person Unicorn Is Coming

This is the column I wrote for the Yorkshire Post this week.

Twenty-five.

That is roughly how many employees Cursor, the AI-powered coding company, had when it crossed one hundred million dollars in recurring revenue. Achieved in twelve months, with no marketing spend, through a product so good that developers simply bought it themselves.

I have spent three decades in technology. I am not easily impressed by revenue milestones. That number stopped me cold.

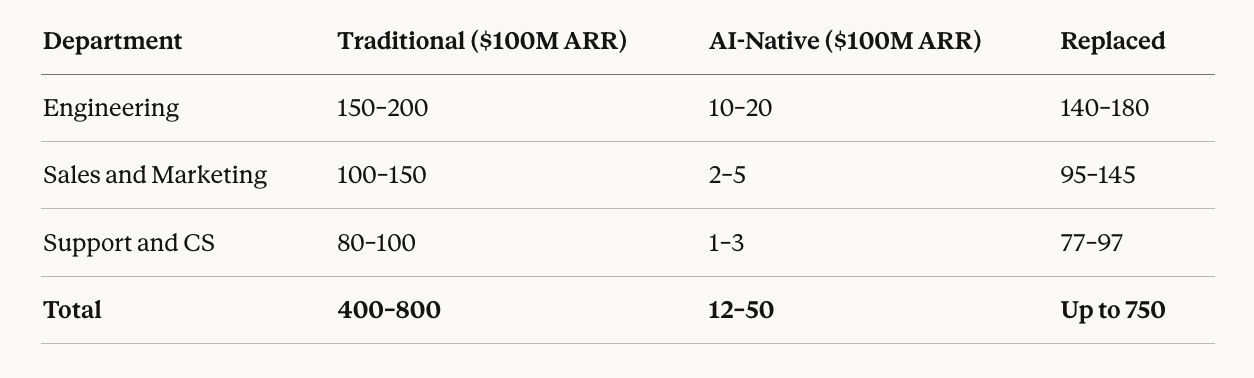

To understand why, remember what £100 million used to imply. A conventional software company reaching that threshold would typically employ between 400 and 800 people. Sales teams chasing pipeline. Customer success managers defending renewals. Marketing operations tracking attribution. Layers of middle management coordinating it all. I have run businesses at that scale. I know what that machinery costs to assemble and to maintain.

Cursor made much of it unnecessary.

And it is not alone.

ElevenLabs closed last year with more than $330 million in ARR. Sierra, founded by Bret Taylor, hit $100 million ARR in seven quarters. Midjourney has shown that an AI-native company can reach extraordinary revenue with a team most corporates would still regard as dangerously lean. The exact ratios vary. The structural shift does not.

That is not incremental improvement. It is structural change.

These businesses were not built as conventional organisations. They were built as automated loops.

Work that once required 200 engineers is now directed by a handful of senior people orchestrating AI agents that write, test and refactor code. Customer support that might have required 100 staff is handled by reasoning systems that check usage logs, interrogate billing records and issue refunds without human intervention. Midjourney does not operate a traditional sales force. It does not need one. Credit card in, product out.

Revenue scales. Headcount barely moves.

The underlying shift is agentic AI. Earlier AI systems summarised and suggested. Useful, but passive. The current generation executes. It builds the feature, runs the tests, deploys the update and handles the complaint. It chains decisions together and improves through feedback. When you map that capability onto a company’s cost base, it does not look like a new tool. It looks like a redefinition of what a company actually is.

For thirty years, growth meant hiring. Hiring meant cost. Cost meant capital. That logic shaped everything from venture funding to office design. Now we are watching leverage detach from labour.

My view is that we are perhaps eighteen months from the first genuine one-person unicorn. A founder directing a fleet of AI systems to build, market and operate a billion-dollar business.

That sounds implausible. So did the idea that a global software company could reach nine figures in recurring revenue with fewer than twenty-five people.

When I started in this industry, launching a product required racks of servers, specialist contractors and months of burn before the first customer invoice. Cloud computing collapsed infrastructure. Modern frameworks reduced development friction. No-code tools shrank teams further. Each wave removed a reason to hire.

Agentic AI may remove the assumption that you need a team in the traditional sense at all.

That should concentrate minds.

Every business leader faces the same uncomfortable question. Are you building for the world that existed five years ago, or the one arriving at speed? The unicorns of the next decade will not be defined by the size of their workforce. They will be defined by the scale of their leverage.

The army, in many cases, has already become the liability.

Story Two: This Is How They Are Actually Doing It

The question everyone asks next is straightforward. How?

The answer matters because these companies are not using AI as a feature bolted on to a conventional business. They have built what the industry now calls an AI-native architecture. The distinction is fundamental. In a traditional company, the software is a tool and the people do the work. In an AI-native company, the agents do the work and the people set the direction.

The result is that human employees have become the bottleneck, not the engine. A small team of senior architects. A fleet of agents executing. No meetings required for the agents to coordinate.

Here is how it plays out in the two departments that consume the most headcount in any growing technology company.

Software Development: The Agentic Fleet

In a traditional company, developers write code. In an AI-native company, developers direct agents that write code.

The directional numbers are striking. Reports from inside companies like Cursor suggest that a significant proportion of the pull requests merged into their product are now created by autonomous AI agents running in the cloud. A small team of architects defines the problem, sets the constraints and spins up fleets of agents working in parallel. Far fewer junior engineers are needed for repetitive, structural work.

When a bug is detected, an AI agent automatically creates a virtual machine, reproduces the bug, writes the fix, and presents a recording of the fix to the human architect for a thirty-second approval.

The industry has coined a term for the developer working this way: vibe coding. A developer describes a high-level intent: “make the checkout flow handle crypto and send a Slack alert”. The AI then manages the thousands of lines of code required to make it happen. The developer never touches the implementation.

The revenue trajectory tells you what this produces. A traditional SaaS company at £100 million ARR employs around 500 people, generating roughly £200,000 per head. Cursor has crossed $1 billion in annualised revenue at a scale of headcount that would once have looked absurdly small. Lovable reached $100 million ARR within eight months of launch and has continued climbing fast.

The point is not the exact spreadsheet ratio. The point is that AI-native companies are scaling output far faster than headcount. The difference is not better engineers. It is a different organisational architecture.

Human replacement estimate: The agentic fleet replaces roughly 150 to 180 junior and mid-level engineers who would otherwise be responsible for boilerplate code, manual testing and bug fixing.

Marketing: Programmatic Growth

Traditional marketing is people-heavy because it requires constant content creation, manual outreach and complex attribution tracking. Lean AI companies have replaced this with what researchers call autonomous growth loops.

Three techniques dominate.

AEO: Answer Engine Optimisation. One or two people use AI to ensure their product is the top recommendation when a potential customer asks ChatGPT, Gemini or Perplexity for advice. They do not write blog posts for humans. They build knowledge graphs for AI. This is rapidly becoming the 2026 version of SEO, and most marketing teams have not yet understood it exists.

Content atomisation. Instead of a social media team, agents take one piece of source content (a founder’s technical talk, say) and automatically produce 50 or more localised videos, posts and ads, each adapted for different markets and platforms. A single piece of original thinking becomes a global content operation without a single additional hire.

The invisible sales force. Midjourney and Cursor have scaled to hundreds of millions in revenue with no traditional sales force. For companies that do need outbound, AI agents now monitor the web for trigger events (a competitor raising prices, a target company hiring aggressively) and automatically generate personalised demos or sequences for every affected prospect. No SDR required.

Human replacement estimate: This replaces 40 to 60 staff across marketing operations, SEO, content creation and sales development. One GTM engineer now does the work of an entire traditional marketing department.

The combined picture is stark.

Story Three: The Exact Tools They Use

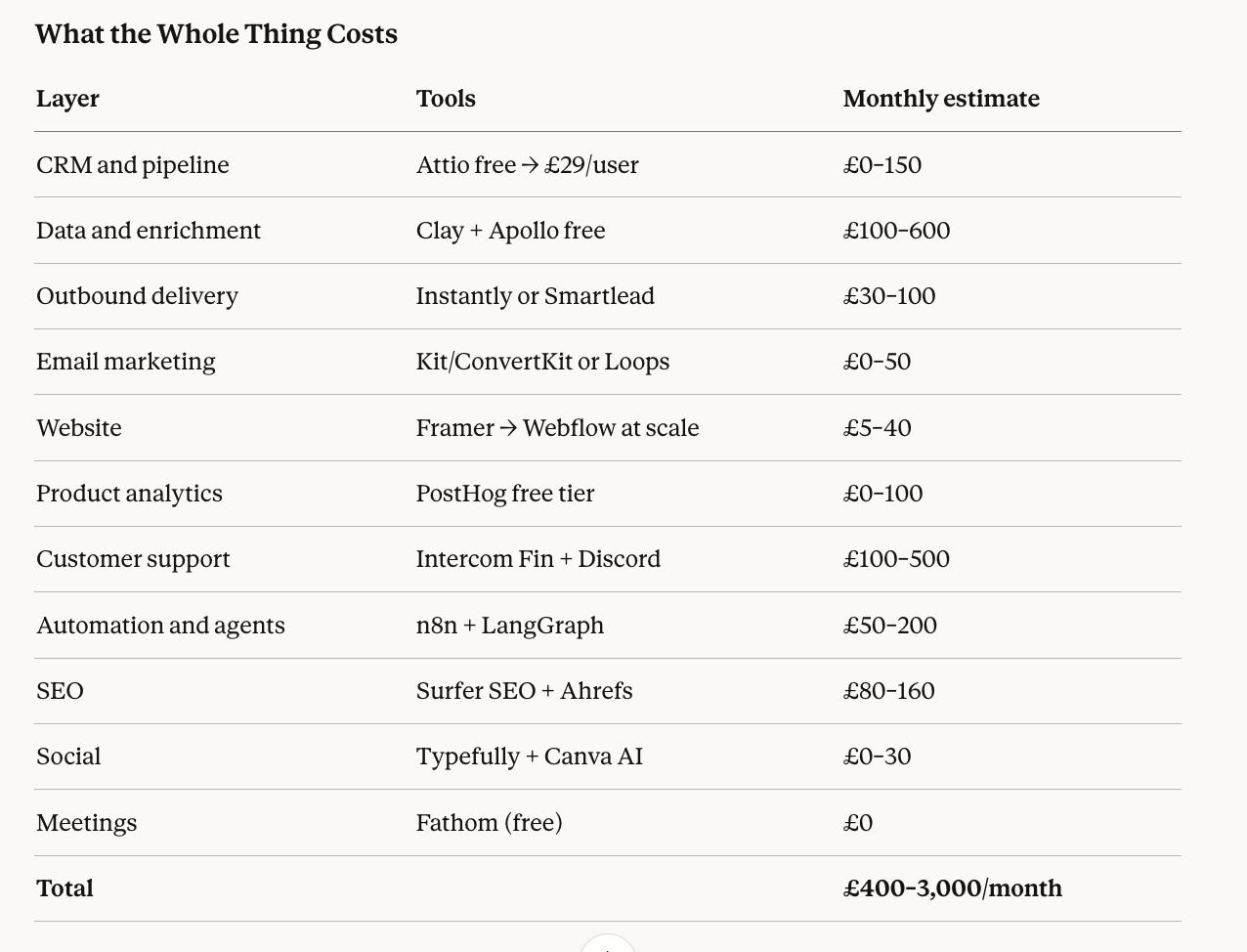

The research is now deep enough to be specific. Based on verified implementations documented across a16z Speedrun, SaaStr, Growth Unhinged and company disclosures, here is what ultra-lean AI companies actually deploy, and what it costs.

The single most important principle before the tools: the most successful lean companies consolidate aggressively. Five to ten core tools rather than thirty. Every additional tool creates coordination cost and cognitive load. The savings are reinvested in AI agent quality.

The Core Stack

Sales and prospecting

The dominant documented pattern is a three-tool combination: Apollo for prospecting (270 million verified contacts, free starting tier) → Clay for enrichment → Instantly for delivery.

Clay itself has crossed $100 million ARR and sits at the centre of nearly every documented lean GTM stack. It is to modern GTM what Salesforce was to the previous era. Its waterfall enrichment sequentially queries 100 or more data providers to maximise contact coverage. OpenAI’s own GTM team used Clay to double contact coverage from 40 per cent to 80 per cent. Rippling used it with hiring data triggers and doubled cold email performance year-on-year.

One GTM engineer running this combination can manage thousands of personalised prospects per week.

CRM

Attio (free to start, £29 per user per month) is the documented recommendation from the a16z Speedrun minimum viable stack. HubSpot free tier for maximum accessibility and zero commitment.

Content and marketing

ChatGPT and Claude serve as foundational writing tools. Midjourney, Runway and Canva AI combined eliminate the need for creative hires entirely. Typefully handles lean social publishing on X and LinkedIn.

Customer support

Intercom Fin has become the default AI support agent for AI-native companies. Fin (powered by Claude) resolves 51 per cent of queries on average without any human involvement. Gamma uses it to resolve 75 per cent of queries end-to-end for 50 million users. Anthropic itself chose Fin over building its own support agent.

Discord runs alongside Fin as the community hub. Midjourney built its entire business on Discord: 2.7 million members serving simultaneously as distribution channel, support platform and product interface.

Product analytics

PostHog has emerged as the consolidation play, replacing Amplitude, LaunchDarkly, Hotjar and Segment in a single platform. Free tier includes one million events per month. Documented users include Supabase, Lovable and ElevenLabs.

Automation backbone

n8n (178,000 plus GitHub stars, self-hostable, from £50 per month) is the standout tool for lean teams. It handles the workflow automation that once required a dedicated DevOps team. One Montreal startup documented using n8n to build an automation backbone typically requiring three or four dedicated operations staff.

AI agents and orchestration

For developer-led orchestration, LangGraph handles complex agent workflows with cycles, conditionals and state persistence. CrewAI ($18 million Series A, 100,000 plus agent executions per day) uses a role-based model for multi-agent coordination. For no-code orchestration, Lindy.ai positions as “AI employees” with pre-built templates for sales, support and recruiting, starting at £29 per month.

What the Whole Thing Costs

For under roughly £3,000 a month, a founder can now assemble a surprisingly capable commercial and operating stack. That does not guarantee a £100 million business. It does mean the cost of trying has collapsed.

The final insight from the research comes from Lenny Rachitsky: your job as a founder is to become world-class at one primary growth engine before layering anything else on top. The tool list above is not a shopping list. Pick the single motion that fits your business. Build it. Own it. Only then add the next layer.

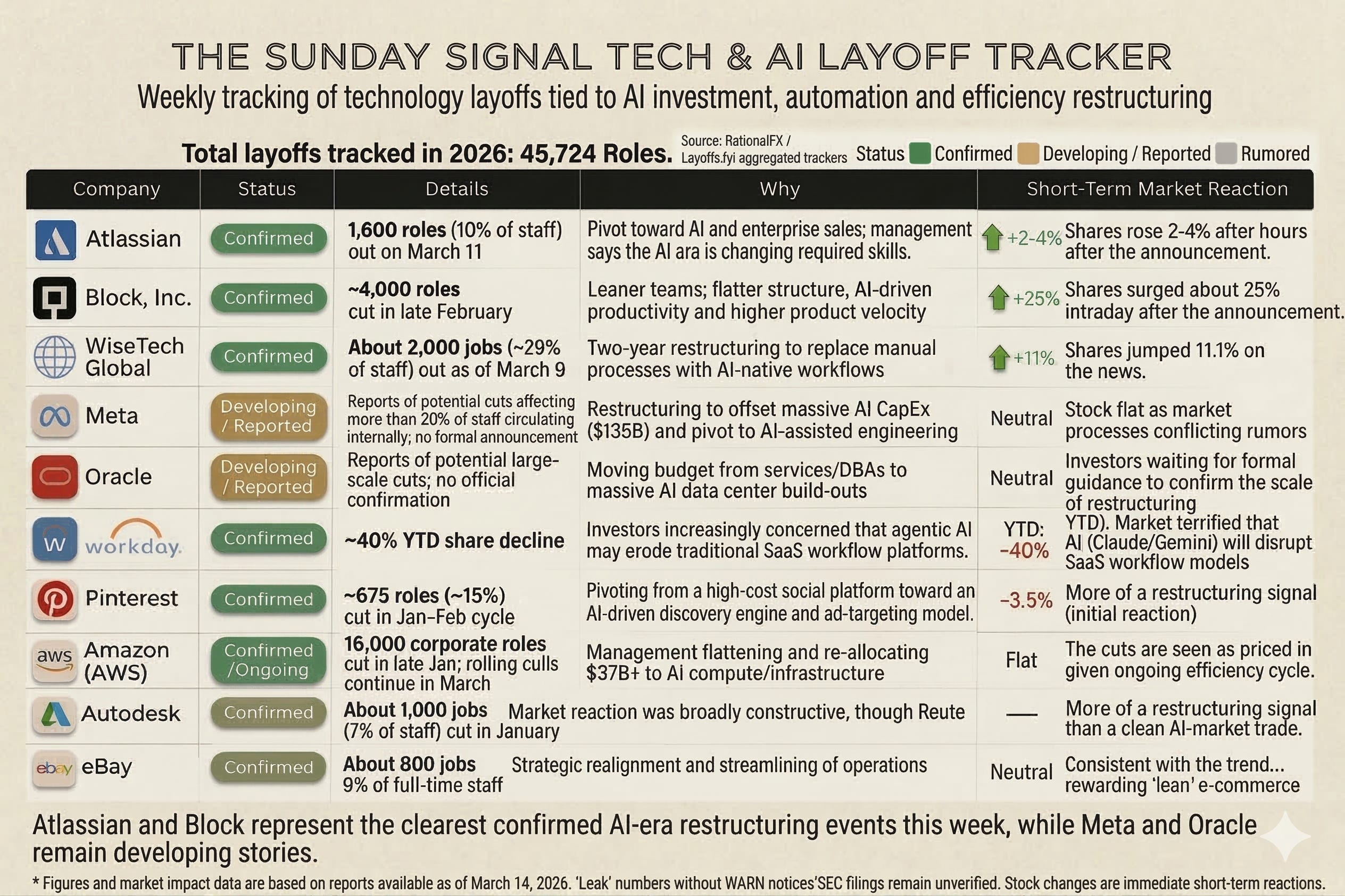

📊 New Weekly Section: The Sunday Signal Tech and AI Layoff Tracker

Since Issue #40 on 8 February, I have been tracking the acceleration of tech layoffs. Issues #41, #42, #43 and last week’s #44 each added more data. The scale now demands a permanent weekly section. From this week, the Tracker runs every Sunday.

In the first eleven weeks of 2026, major tech companies have announced or are developing cuts totalling approximately 45,724 roles, according to tracker-based estimates from RationalFX and Layoffs.fyi. The unverified and developing stories suggest the real figure may be considerably higher.

But the raw totals are the least interesting part of the story. The patterns are what matter.

Pattern one: the AI pivot premium is real

The market is explicitly rewarding companies that announce they are cutting people to fund AI investment.

Atlassian cut 1,600 roles (10 per cent of staff) on 11 March and the stock rose approximately 4 per cent. Investors cheered the pivot from growth-at-all-costs to AI efficiency. WiseTech Global cut roughly 2,000 roles (30 per cent of staff) to replace manual coding with AI-native workflows. Share price up 11 per cent.

Block went furthest. Roughly 4,000 roles eliminated in a massive shift to AI-augmented lean teams and to reverse what the company described as the 2018-to-2024 bloat. The result was one of the largest single-day market cap gains in Block’s history, up approximately 25 per cent.

The signal is clear. Investors are not mourning the jobs. They are pricing in the leverage.

Pattern two: the SaaS crisis is emerging

Not every company is being rewarded for its AI pivot.

Workday cut 400 roles in customer operations in February. The stock is down around 40 per cent year to date. The reason is not the number of cuts. The reason is investor fear that agentic AI will not just assist Workday’s enterprise software. It may make the software itself unnecessary.

If developers stop writing structured HR workflows and instead describe what they want to an agent (the vibe coding model), then the value of a heavyweight enterprise HR platform collapses. Investors are beginning to ask whether tools like Workday remain as indispensable in an agentic world as they looked in the last software cycle.

This is the deepest structural risk I have been writing about since Issue #40. The AI disruption is not symmetrical. Companies building AI infrastructure are gaining. Companies that were built on the assumption of human cognitive labour are the ones in danger.

Pattern three: rumour versus reality

Not every number circulating in tech forums is confirmed.

Meta has reports of potential cuts affecting more than 20 per cent of staff circulating internally, with no formal announcement and no SEC filing to date. Oracle reports suggest potential large-scale cuts are developing; no official confirmation has been given. Treat both as directional signals until they appear in a regulatory filing, not as settled facts.

Amazon is confirmed. 16,000 corporate role reductions, framed explicitly as management flattening and a reallocation of $37 billion to AI compute and infrastructure. That one is in the numbers.

Pinterest cut 675 roles (approximately 15 per cent of staff) in a January/February cycle to pivot from a high-cost social platform to an AI-driven discovery engine. Stock down 3.5 per cent on the initial reaction, with recovery building as AI-targeting optimism grows. Autodesk cut approximately 1,000 roles (7 per cent) to reorganise around AI-driven generative design tools. eBay has confirmed approximately 800 roles, 9 per cent of full-time staff, in a strategic realignment.

Figures and market impact data are based on reports available as of 14 March 2026. Tracker estimates sourced from RationalFX and Layoffs.fyi. Developing stories without WARN notices or SEC filings remain unverified. Stock changes are immediate short-term reactions.

🚀 Final Thought

The army, in many cases, has already become the liability.

The one-person unicorn is not a thought experiment. It is an engineering problem. And several people are very close to solving it.

When I started in this industry, launching a product required racks of servers, specialist contractors and months of burn before the first customer invoice. Cloud computing collapsed infrastructure. Modern frameworks reduced development friction. No-code tools shrank teams further. Each wave removed a reason to hire.

This wave may remove the assumption entirely.

The question is not whether this is coming. It is whether you are on the right side of the shift.

David Richards MBE is the co-founder of Yorkshire AI Labs. He writes a weekly column for the Yorkshire Post and is a regular commentator on technology, business and the future of work.

The Sunday Signal is produced as a weekly podcast using a voice cloned from David’s own voice, a demonstration of the same AI capabilities he writes about. Listen on Spotify, Apple Podcasts, and YouTube.

Until next Sunday, David

This should go viral.