The Sock Puppet Is Back. This Time It Is Wearing a Suit.

Why the AI era rhymes perfectly with every great disruption in history, who the real losers are, and an investor's guide to separating the signal from the noise | Issue #50 | Sunday, 19 April 2026

This issue is also available as a podcast. Listen on Spotify, Apple Podcasts or YouTube and tell me what you think.

Bottom Line Up Front

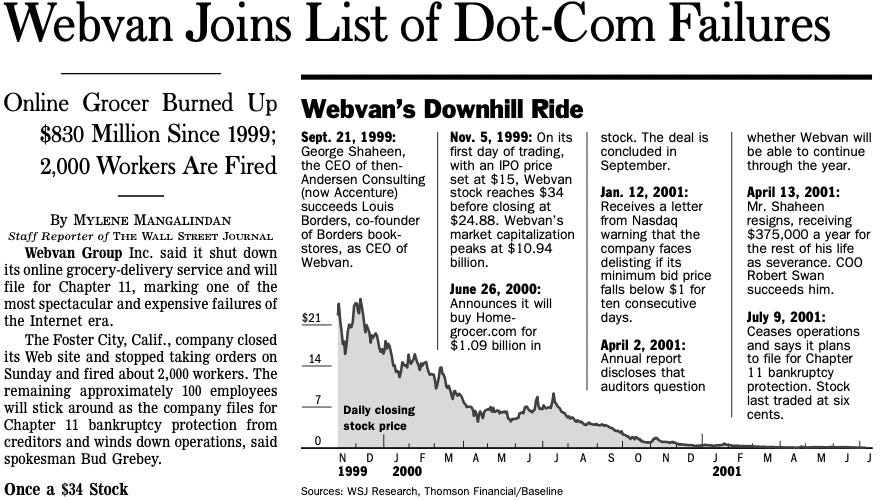

History does not repeat itself. But it borrows the same costume every time. Last Friday I wrote in the Yorkshire Post about clearing out my garage and finding a Webvan stress ball, a Yahoo! mousepad, and an Ariba t-shirt. Those artefacts of the dot-com era cost investors hundreds of billions of pounds. The companies behind them died. The infrastructure beneath them did not. It became the plumbing for everything that followed.

The AI era is doing exactly the same thing. The pattern is identical. The displacement is real. The casualties are already bleeding. And an alarming number of fund managers and company executives are standing at the podium this earnings season with straight faces, telling investors that AI is helping their business. Most of them are wrong. Some of them know it.

This week, on the fiftieth issue of The Sunday Signal, we examine three things. First, what the sock puppet actually taught us, and why the lesson applies right now. Second, the full sweep of technology disruption across forty years, told honestly, without the survivor bias that distorts every boardroom presentation. Third, an investor’s guide with a concrete hot list: who is truly insulated, who is already dying, and why the most dangerous sentence in finance right now is “AI is helping everyone.”

1. The Sock Puppet Never Changes. Only the Sock Does.

In my column in the Yorkshire Post on Friday, I described unearthing a collection of dot-com relics from my garage. The Pets.com sock puppet. The Webvan stress ball. The Ariba t-shirt. I dropped the lot in the recycling bin. The lesson, I wrote, is not so easy to dispose of.

The Super Bowl in January 2000 remains the most instructive single moment in the history of technology investment. Fourteen separate dot-com companies each paid around two point two million dollars for thirty seconds of airtime. Pets.com sent a sock puppet. The company was bankrupt nine months later.

That game was not the peak of innovation. It was the peak of theatre. The revenues were not there. The margins were not there. In many cases every transaction lost money. The business model was not merely deferred; it had never existed.

Here is what people consistently misremember about that era. The collapse of Pets.com, Webvan, and Kozmo was not evidence that the internet was overhyped. It was evidence that speculative capital had attached itself to weak models. Amazon survived. Google survived. The fibre-optic cables that were laid at extraordinary cost during that period became the arterial infrastructure for the modern internet. The disruption was real. The casualties were selective.

There is a direct application to 2026.

Ask yourself this: of the companies you have invested in, partnered with, or work for, how many are the Pets.com of this cycle? They have raised money. They have a plausible story. They have a sock puppet, or the modern equivalent, which is a beautifully designed AI dashboard that wraps around a database and charges per seat per month.

The comparison I drew in the Yorkshire Post column is worth sharpening here. At its peak, Ariba was trading at over one hundred times its annual revenue, with investors paying for cash flows that never materialised. Cisco, the infrastructure darling of the era, peaked at twenty-six times sales. Now consider Anthropic: founded in 2021, already trending towards thirty billion dollars in annualised revenue, and trading at roughly thirteen times that figure. The multiple on genuine AI infrastructure is lower than the multiple on speculative dot-com theatre was at its peak. That is not a bubble. That is a structural repricing of computing power.

But Ariba is not the story. Ariba is the cautionary tale. The story is what survived. The entrepreneurs who built on that speculative infrastructure after the crash, buying assets at pennies in the pound, created the most valuable companies in human history. Around that same genuine foundation today, a second layer of companies has grown up that has no more durable a moat than Pets.com had. Their business model is not innovation. It is theatre.

Anthropic is not the risk. The risk is the company presenting to you this week with a ChatGPT wrapper and a go-to-market slide that describes itself as an AI-powered platform. Strip out the AI language and what you have left is a project management tool with a chatbot bolted on and a per-seat subscription model heading directly into the SaaSpocalypse.

The sock puppet is back. This time it is wearing a suit. And it is presenting at your next board meeting.

2. The Pattern of Destruction Is Always the Same. Only the Technology Changes.

To understand who loses in the AI era, you have to understand who lost in every previous era, and why. The mechanism of displacement does not change. Only the underlying technology does.

The Mainframe-to-PC Era: The Unbundling of Power

In the early 1980s, Digital Equipment Corporation was the second-largest computer company in the world. It employed over one hundred thousand people. Its founder, Ken Olsen, had famously said in 1977 that there was no reason for any individual to have a computer in their home. By 1992 the company was haemorrhaging cash. By 1998 it had been absorbed by Compaq. Compaq itself was absorbed by Hewlett-Packard three years later.

Wang Laboratories was making a billion dollars a year selling word-processing systems to enterprise clients. It filed for bankruptcy in 1992. Prime Computer, Data General, and a dozen other mainframe-era giants either collapsed or shrank into irrelevance inside a decade.

The mechanism was simple. Microsoft and Intel decentralised computing. They standardised the components. They shifted power from hardware gatekeepers who charged enormous sums for vertically integrated systems to a software layer that sat on top of commoditised hardware. The mainframe companies were not slow-witted. They were structurally compromised. Their business model depended on lock-in that the PC dissolved.

The winners did not win because they were clever. They won because they owned the standard. Microsoft owned the operating system. Intel owned the processor. Cisco owned the network that connected the machines. These were infrastructure bets, not product bets.

The Web Era: The Disintermediation of Everything

The World Wide Web did not create new products. It eliminated the friction between buyers and sellers that entire industries had monetised for decades.

Borders had over four hundred stores and a market capitalisation of over two billion dollars in 1999. It filed for bankruptcy in 2011, liquidating over ten thousand jobs. Blockbuster had nine thousand stores globally and employed sixty thousand people. The thing that killed it was not technology, precisely. It was the willingness of Netflix to absorb short-term losses to acquire long-term customer lock-in. Blockbuster had multiple opportunities to buy Netflix. It declined.

The travel agent industry collapsed not because travel stopped but because Expedia and Kayak eliminated the information asymmetry that travel agents had monetised for generations. Why would you pay a human being to search databases you could search yourself?

Sears is the most instructive casualty. It invented the catalogue retail model in the nineteenth century. It was, by any reasonable definition, the Amazon of its era. It had the scale, the supply chain, and the customer trust. What it lacked was the willingness to cannibalise its physical estate before Amazon did it for them. Its market capitalisation peaked at over twenty billion dollars. It filed for bankruptcy in 2018.

The mechanism: in every web-era casualty, the company’s core value proposition rested on control of a physical chokepoint, whether that was a high street location, a proprietary database, or an information advantage. Digital distribution eliminated all three.

The winners: Amazon, Google, eBay, PayPal. Not because they were braver. Because they had no physical chokepoint to defend.

The Mobile and Cloud Era: Ubiquity Kills Category Leaders

Nokia had forty-one per cent of the global mobile phone market in 2007. In 2013 it sold its handset division to Microsoft for five point four billion euros. Microsoft wrote down nearly all of it within two years.

BlackBerry built its brand on security and the physical keyboard. By 2016 it had less than one per cent market share. The product was genuinely superior for its designed purpose. The market changed the purpose.

Sun Microsystems had revenues of over eighteen billion dollars at its peak. Its co-founder Scott McNealy famously said the network is the computer. He was right. What he did not foresee was that Amazon Web Services would commoditise the hardware layer that Sun depended upon. Sun was acquired by Oracle in 2010 for seven point four billion dollars, a fraction of its peak valuation.

The winners of the cloud era were those who provided the infrastructure of ubiquity. Apple owned the device. AWS owned the server. Netflix owned the content pipe. Spotify owned the audio pipe. They all won because they converted occasional purchases into permanent dependencies.

The AI Era: Cognitive Labour Is the New Friction

The mechanism in the AI era is the commoditisation of cognitive labour and autonomous execution. The losers are those whose business model depends on charging for tasks that a large language model or an autonomous agent can now execute instantly, at near-zero marginal cost, in fifty languages, without a salary, without HR infrastructure, and without sleep.

That is not a marginal threat. It is an existential one. And the companies most exposed are precisely those that spent the last decade convincing investors that recurring subscription revenue made them permanently safe.

3. The Investor’s Guide: Why “AI Is Helping Us” Is the Most Expensive Lie in the Room

Here is something you should try at your next investor meeting.

Ask the companies being presented to you whether AI is helping their business. Nearly all of them will say yes. The managing partner will nod. The deck will include a slide about AI productivity gains. There will be a number, probably expressed as a percentage of efficiency improvement, that has been produced by a consultant and approved by the communications team.

Most of it is nonsense.

The Bank of America Fund Manager Survey from late 2025 found that 53 per cent of surveyed investors already believe AI is increasing productivity. That sounds encouraging until you read the next finding: the same survey identified the AI bubble as the number one biggest tail risk for the economy and markets, cited by 45 per cent of investors. More than half believed AI stocks were in a bubble. The most crowded trade in the market was Long Magnificent Seven, held by 54 per cent of fund management survey participants. What this tells you is that the professional investment community simultaneously believes AI is productive, AI is a bubble, and AI stocks are the most crowded trade available. That is not a coherent investment thesis. It is a collective refusal to make a decision.

AI cannot help everyone. That is mathematically impossible. The productivity gains being achieved by AI-native companies are coming at someone’s expense.

Let me give you the honest version.

The SaaSpocalypse Is Not Over

As I covered in recent issues of The Sunday Signal, February 2026 delivered what traders at Jefferies immediately christened the SaaSpocalypse. Triggered by the Claude Cowork product launch, it erased an estimated one trillion dollars in software market capitalisation as investors concluded that AI agents would disrupt the traditional SaaS business model.

The software as a service price-to-earnings multiple has compressed from 84.1 times during the 2020 to 2022 peak to just 22.7 times by March 2026. That is not a correction. That is a structural revaluation.

Recent surveys indicate that 40 per cent of IT budgets are being reallocated from traditional SaaS subscriptions to agentic platforms and large language model token usage.

The mechanism is brutal and simple. If one AI agent can perform the work of five human employees, a company only needs to pay for one software seat instead of five. That seat compression is no longer a theoretical risk. It is a line item in the 2026 budget of every major enterprise.

The Hot List: Companies Already Dying

These are not speculative predictions. These are companies whose business models have been structurally compromised and whose valuations reflect the market’s verdict.

Fiverr (FVRR). The thesis was simple: connect buyers with freelance digital labour. FVRR shares have lost more than sixty per cent of their value over the past year. The company’s full-year 2026 guidance projects revenue declines of anywhere between twelve per cent and three per cent, against analyst expectations that were substantially higher. The barrier to entry for acceptable digital creation has effectively collapsed. A blog post that cost fifty dollars and three days on Fiverr now costs fractions of a penny and three seconds from an AI model. The platform is not being disrupted. It is being deleted.

In 2026 alone, FVRR is down over fifty per cent while the S&P 500 is down just seven per cent.

Teleperformance (TEP.PA). The world’s largest business process outsourcing company employed hundreds of thousands of people globally to staff call centres. Klarna publicly announced that its AI assistant has handled two thirds of its customer service chats since launch, doing the equivalent work of seven hundred full-time human agents with higher satisfaction scores and a twenty-five per cent drop in repeat enquiries. Teleperformance’s share price has declined by over seventy per cent from its peak. Short interest has risen to 6.4 per cent of the stock available for trading, well above the 2.4 per cent average for European technology-services companies. The market is pricing in terminal decline.

Chegg (CHGG). The original canary. A company that sold textbook answers and homework help at the price of a monthly subscription. The stock has fallen from over one hundred dollars to below one dollar. There is no pivot available. The product was the answer. The answer is now free.

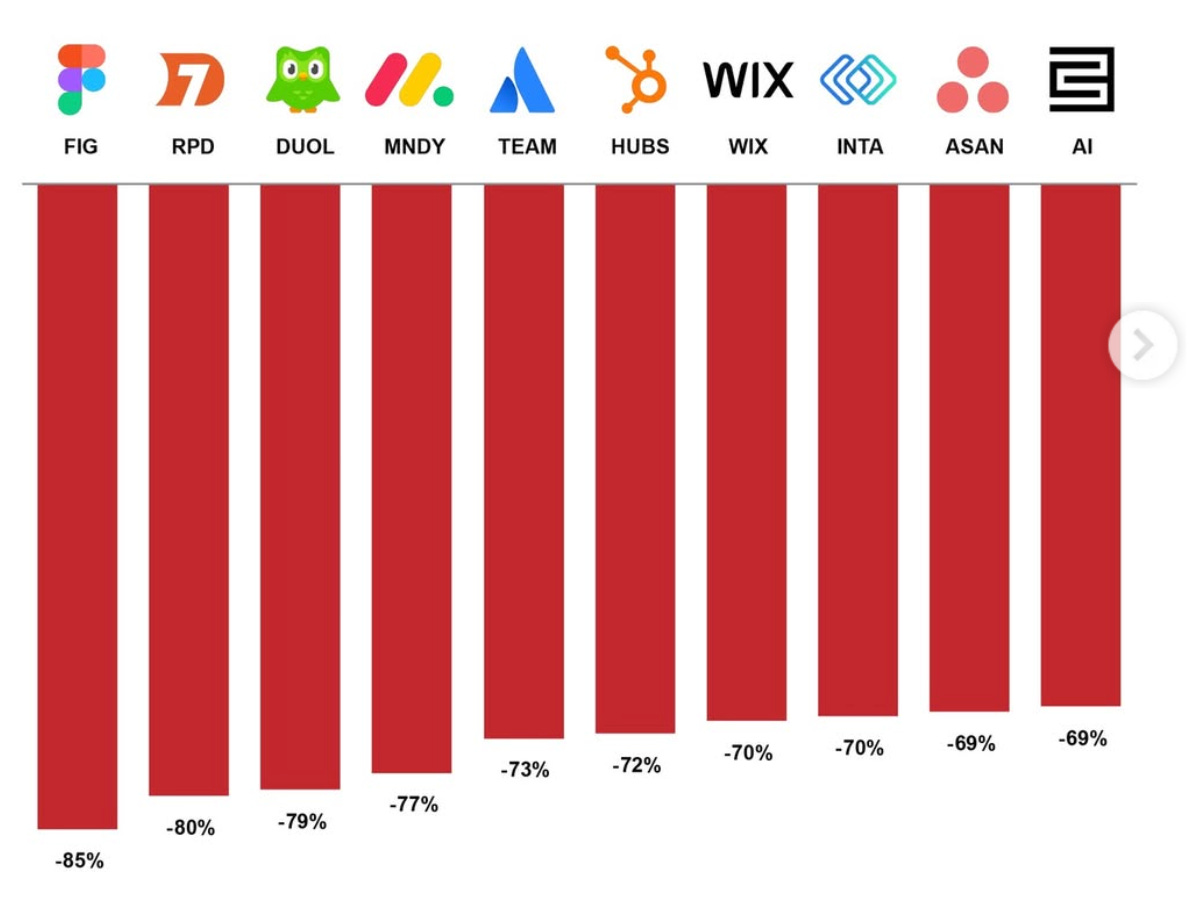

Generic SaaS platforms. Atlassian is down 35 per cent and Salesforce down 28 per cent as their core workflows, task tracking, data entry, and customer logging, are precisely what AI agents automate best. The per-seat model that powered twenty years of software growth is breaking. If ten AI agents do the work of one hundred sales representatives, companies need ten Salesforce seats, not one hundred.

The Hot List: Companies That Cannot Be Touched

The companies that survive technological disruption have one of three things: proprietary data that cannot be replicated, infrastructure that is physically irreplaceable, or software so deeply embedded in legal and compliance processes that ripping it out would cost more than the disruption itself.

Nvidia (NVDA). The picks-and-shovels play of the AI era. Every foundation model, regardless of who builds it, runs on Nvidia silicon. They are the tollbooth. Their revenue is not a bet on one company winning the AI software war. It is a bet on the war continuing, which it will.

RELX (REL.L). Owns LexisNexis and Elsevier. Initially sold off by investors who assumed ChatGPT would destroy its legal and scientific research platforms. The market was wrong. RELX owns decades of legally aggregated, deeply verified, proprietary data. A hallucinating generalist AI model cannot be used in a court case or a medical trial. RELX’s data can. It is now charging premium prices for AI tools trained on information the open internet does not contain.

The Sage Group (SGE.L). The accounting and payroll software that underpins British businesses. You cannot rip out the software that manages your legal financial compliance simply because a new AI agent exists. Sage is a vertical system of record. Its customers are locked in not by preference but by obligation.

TSMC. The company that physically manufactures the chips that Nvidia designs. Software is eating the world. TSMC owns the teeth.

The Survival Rule

History is consistent on this point. The companies that survive a technological transition are not the ones who embrace the technology loudest. They are the ones who own something the technology needs to function.

In the PC era, that was the microprocessor and the operating system. In the web era, it was the distribution network and the trust relationship with the consumer. In the cloud era, it was the physical server and the fibre connection. In the AI era, it is the proprietary data that AI models cannot scrape, the physical infrastructure that AI models cannot exist without, and the regulatory compliance that AI models cannot substitute for.

If the company you are evaluating does not own one of those three things, the fact that they put an AI slide in their board deck is not reassuring. It is concerning.

A Note for British Investors

The UK equity market provides a concentrated case study. WPP (WPP.L), one of the world’s largest advertising agency networks, is trading around 267 pence, having fallen from a 52-week high of over 616 pence. That is a decline of roughly fifty-six per cent. The market is not punishing WPP for poor management. It is repricing the fundamental economics of selling billable creative hours when generative AI can do the same work in seconds. Keywords Studios, once a darling of the London market for its outsourced video game development services, was delisted entirely in October 2024 after private equity stepped in to take the business off the public market’s brutal scrutiny.

Meanwhile, Arm Holdings (ARM), Cambridge-born and New York-listed, sits precisely where every infrastructure play has sat in every previous disruption cycle. It designs the chip architecture that powers virtually every mobile device on earth and increasingly every AI data centre. It does not care which AI software company wins the war. All of them run on Arm’s architecture. This is the Cisco of the AI era.

British businesses and British investors need to ask themselves an honest question. The dot-com era built the infrastructure that benefited Amazon and Google. The cloud era built the infrastructure that benefited American hyperscalers. Is British capital and British enterprise positioned to own the infrastructure of the AI era, or is it once again positioned to be a consumer of it?

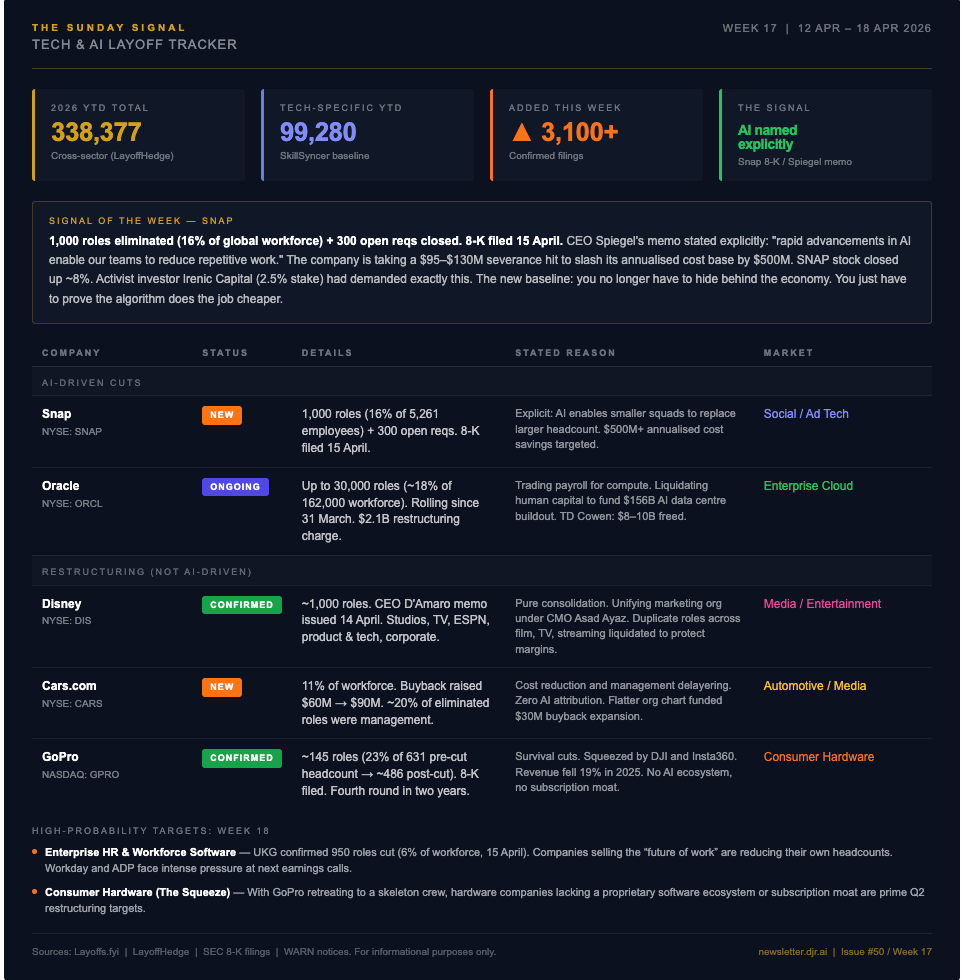

The Sunday Signal Tech & AI Layoff Tracker | Week 17 | 12 April – 18 April 2026

Signal of the Week: Snap Says the Quiet Part Out Loud. Snap filed an 8-K confirming the elimination of 1,000 roles (16% of its global workforce of 5,261) and the closure of 300 open requisitions. CEO Evan Spiegel’s memo stated explicitly that “rapid advancements in artificial intelligence enable our teams to reduce repetitive work.” The company is taking a $95–$130 million severance hit to slash its annualised cost base by $500 million. SNAP stock closed up approximately 8 per cent. Activist investor Irenic Capital (2.5 per cent stake) had been demanding exactly this move. The new baseline: you no longer have to hide behind the economy. You just have to prove the algorithm does the job cheaper.

Sources: Layoffs.fyi, LayoffHedge, SEC 8-K filings, WARN notices. For informational purposes only.

🚀 Final Thought: The Lesson Is Always Staring at Us

Fifty issues of The Sunday Signal. I have spent most of them arguing that the displacement of cognitive labour by AI is not a future event but a current one. The pattern weavers of the West Riding were told the Jacquard loom was a tool to assist them. Within twenty years there were riots and burning mills and children starving in villages that had supported entire communities through skilled craft. The technology did not stop. The promises made to the workers did not come true.

The story being told this earnings season is one in which AI helps everyone. Productivity goes up. Costs come down. No one loses. Shareholders celebrate. Executives collect their bonuses.

The markets are not buying it. They have already written off the cognitive arbitrage businesses. They have already begun pricing Salesforce and Workday as utilities rather than growth companies. They have already halved the valuations of the companies that connect human labour to digital tasks.

The market is not pessimistic. It is rational.

The dot-com era punished those who paid for theatre. It rewarded those who understood what was genuinely being built beneath the noise. The fibre was real. The data centres were real. Amazon was real. The sock puppet was not.

This era will end the same way. The infrastructure is real. The displacement is real. The companies caught in between, claiming that AI is helping them while their seat counts shrink and their margins compress, are the sock puppet of 2026.

The question is not whether you can spot them. They are standing at the front of the room. The question is whether you act before the bankruptcy filing does it for you.

Until next Sunday, David

The Sunday Signal is published weekly at newsletter.djr.ai. Listen on Spotify, Apple Podcasts and YouTube.